Production records

Practical Action

Stock management

In general, small-scale processors keep the amounts of stored ingredients, packaging and

products to a minimum. Decisions on the size of stocks depend on the balance between the

cost of buying the material and the cost of storing it. The materials that are most likely to be

stored are high-value materials that are used most often and/or they cannot be replaced

quickly. The least likely materials to be stored are the lowest value materials that are used

least often and are readily available and so can be easily replaced.

Storeroom management involves monitoring and controlling material movements into and out

of the stores, and checking stock levels and stock rotation. Bin Cards (Table 11) may be fixed

to containers for easy identification of raw materials, work in progress and finished goods. Also

defective materials such as spoiled foods and foods to be reworked can be identified in this

way.

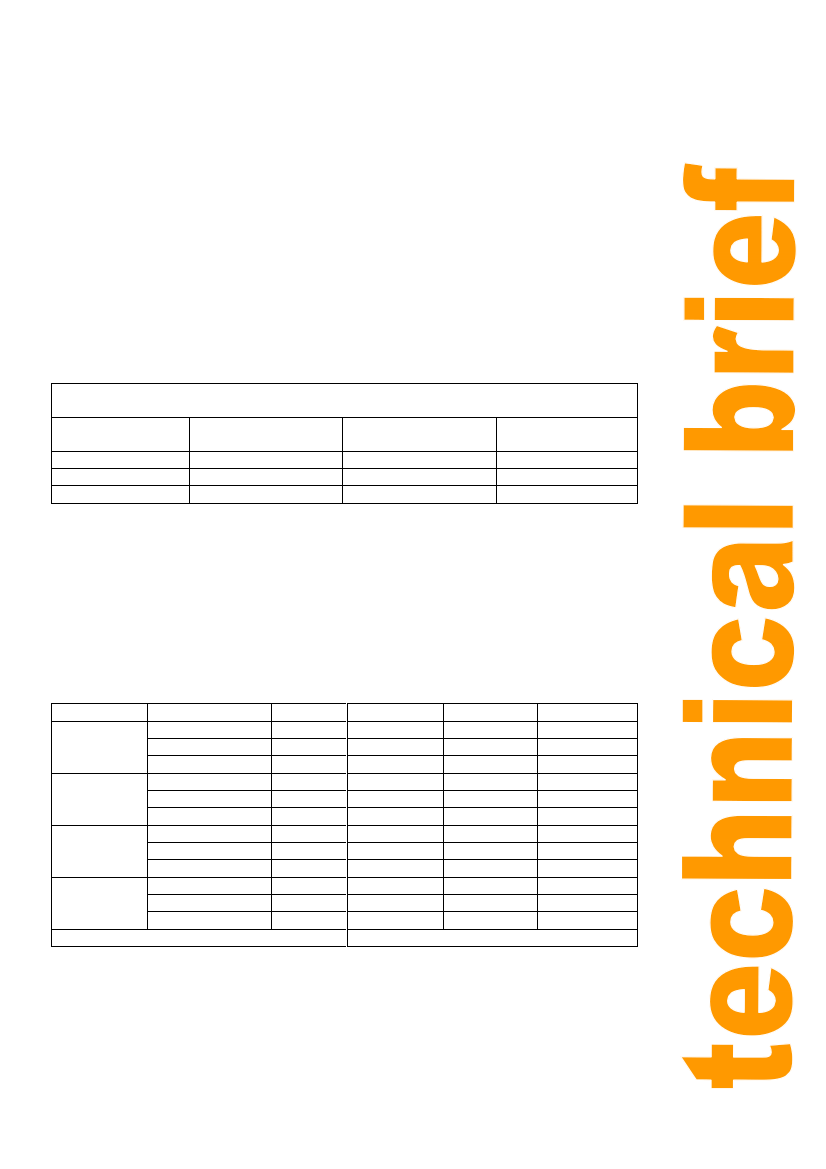

Table 11. Bin card

Item …………………………..

Date

No/Weight/Volume

received

No/Weight/Volume

used

Balance

The Storekeeper carries out a physical stock check at the end of each day and records this on

a Stock Balance Record (Table 12). A full stock check of the amounts of ingredients,

packaging and products is made by the production supervisor at the end of each week and by

the finance officer at the end of each month. The results of these stock checks are also

recorded on the Stock Balance Record and these are given to the owner each month. The

production supervisor also uses the Stock Balance Records to cross-references ingredient

usage with the amount of production each month to confirm that the correct amounts of

ingredients have been used, or to identify if there are any discrepancies that may indicate

pilferage.

Table 12. Stock Balance Record

Date

Ingredient:

Flour (kg)

Expected balance

Actual amount

Variance

Expected balance

Actual amount

Variance

Expected balance

Actual amount

Variance

Expected balance

Actual amount

Variance

Completed by ………………..(Storekeeper)

Oil (litres)

Salt (kg) Colouring (g)

Checked by…..……..(Production supervisor)

7